How Dominant is the U.S. Dollar?

The U.S. dollar has been the world’s dominant currency since the end of World War II.

According to the Congressional Research Service, roughly half of international trade, international loans, and global debt securities are denominated in USD. The same goes for many of the world’s most important commodities including gold, silver, and crude oil.

In this Markets in a Minute chart from New York Life Investments, we provide a snapshot of the U.S. dollar’s global standing.

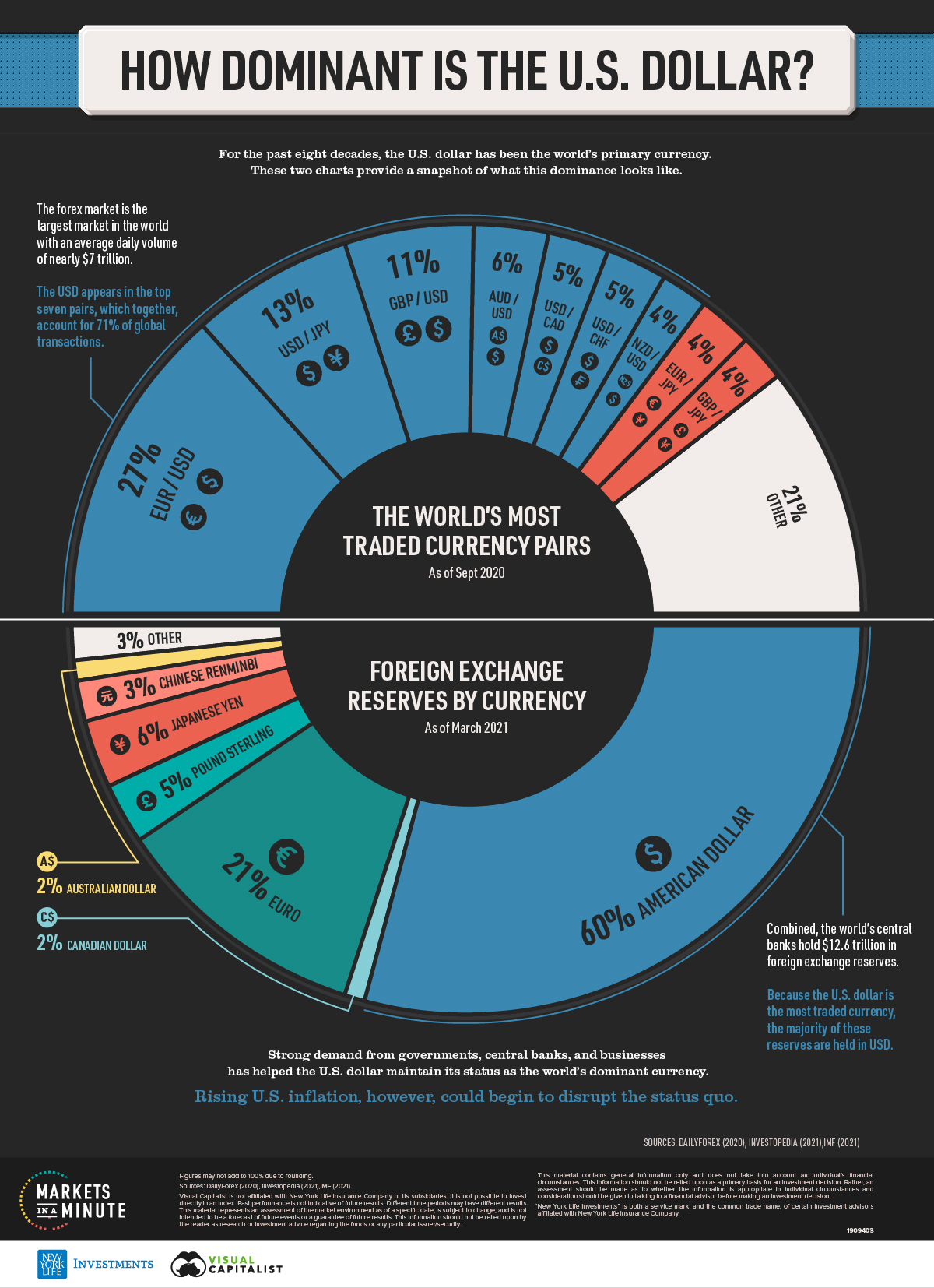

The World’s Most Traded Currency Pairs

The foreign exchange market is the largest financial market in the world, with an average daily trading volume of almost $7 trillion. The majority of this volume is driven by banks, corporations, and other financial institutions.

More than 70% of this volume is generated from the top seven currency pairs, all of which involve the U.S. dollar.

| Currency Pair | Share of Global Transactions |

|---|---|

| EUR/USD | 27% |

| USD/JPY | 13% |

| GBP/USD | 11% |

| AUD/USD | 6% |

| USD/CAD | 5% |

| USD/CHF | 5% |

| NZD/USD | 4% |

| EUR/JPY | 4% |

| GBP/JPY | 4% |

| Other | 21% |

Figures may not add to 100% due to rounding.

The EUR/USD pair is the world’s most traded currency pair and is commonly referred to as “fiber”. It indicates how many U.S. dollars are needed to purchase one euro.

Foreign Exchange Reserves by Currency

Central banks typically hold foreign exchange reserves for purposes such as:

- Influencing exchange rates

- Maintaining liquidity in the event of a crisis

- Backing debt obligations

Given its status as the world’s dominant currency, the USD naturally represents a majority of these reserves.

| Currency | Share of Total Reserves |

|---|---|

| US dollar | 60% |

| Euro | 21% |

| Japanese Yen | 6% |

| Pound sterling | 5% |

| Chinese renminbi | 3% |

| Australian dollar | 2% |

| Canadian dollar | 2% |

| Other | 3% |

Figures may not add to 100% due to rounding.

Japan and China are the world’s largest foreign holders of USD, with stockpiles of over one trillion each. These are often accumulated by purchasing U.S. Treasury bonds, a strategy for devaluing one’s domestic currency.

Because a large portion of China’s GDP is generated from exports, the country benefits when its currency, the renminbi (RMB), is weaker relative to the dollar. A relatively weak RMB means Chinese exports become cheaper than American-made goods.

How Long Will The U.S. Dollar Reign?

Today’s shifting geopolitical and economic landscape presents challenges to the U.S. dollar’s global status.

China has overtaken the U.S. as the world’s major trading partner, and is looking to leverage its power to expand the presence of the RMB. Two factors that limit the RMB’s potential as an international currency are tight government controls and a lack of transparency.

Another threat to the USD’s dominance is the use of financial sanctions, which limit foreign access to the U.S. financial system. While these sanctions may be effective from a foreign policy perspective, they can also undermine the global role of the USD.

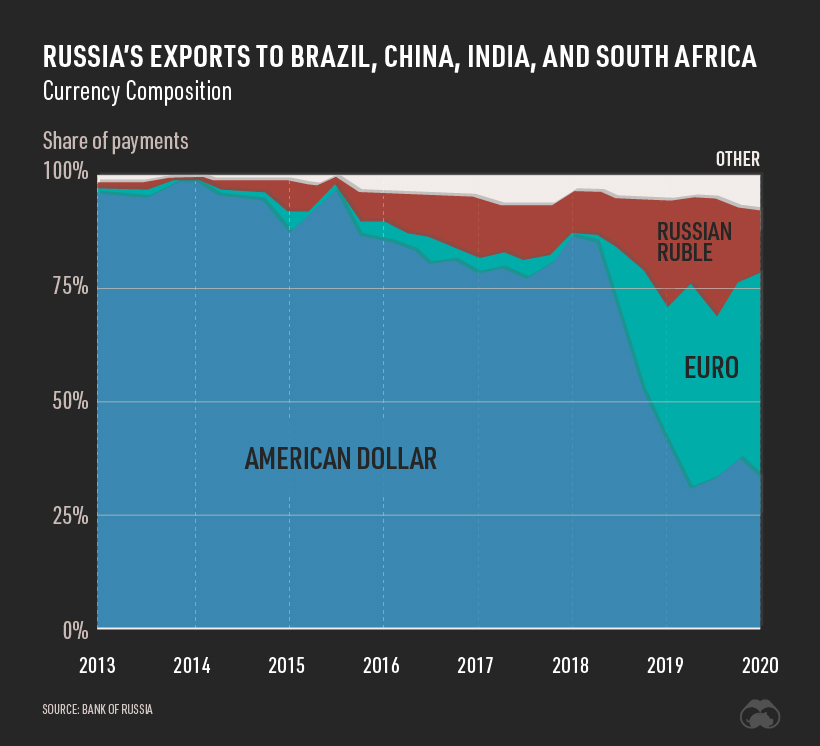

The following chart illustrates how Russia has circumvented the U.S. dollar in the face of American sanctions.

More specifically, Russia and China have been working towards a closer financial alliance. As of Q1 2020, just 45% of trade between the two nations was denominated in USD, down from 90% in late 2015.

What About Inflation?

America’s M2 money supply has grown significantly since the 2008 global financial crisis, and even more so during the COVID-19 pandemic. M2 includes cash, checking deposits, and liquid vehicles such as money market securities.

Looking forward, U.S. inflation is expected to accelerate. In August 2020, the Federal Reserve announced it would switch to an inflation-averaging policy. This means that annual inflation will be allowed to exceed 2% in a given year, so long as the 2% target is achieved over a longer timeframe.

In some respects, higher inflation can be a positive. The U.S. debt to GDP ratio is currently over 100%, and by 2050, it’s expected to reach 195%. With so much debt being issued, sustained inflation can gradually undermine the real value of these liabilities. The tradeoff, of course, is a further weakening of the U.S. dollar.